Understanding corporate landlords: Decoding a recent housing phenomenon

This article is the first in an informational series about corporate landlords. Click here to read the second article, “Understanding corporate landlords: Who are they?,” and click here to read the third article, “Understanding corporate landlords: Where are they in Mecklenburg County?”

The term “corporate landlord” has gained significant attention across the United States in the last few years. Yet, despite all the news stories and legislation focusing on these entities, you may find yourself puzzled by the hype around them or how they relate to your community. You may even be asking yourself:

- Who are corporate landlords?

- What makes corporate landlords controversial?

- How many corporate landlords are there in Charlotte-Mecklenburg?

- Why do corporate landlords matter for Mecklenburg County or Charlotte?

The uncertainty surrounding corporate landlords is not that surprising. While these landlords have existed for decades, they only came into the public consciousness after the Great Recession in 2008 drastically altered the real estate market and made it easier for large corporations to purchase homes in bulk (Lopez & Kattan & Ash, 2022; Yeakey 2024). We therefore take a closer look at these entities in a new, multi-part series that addresses and explores the questions outlined above. We aim to share with residents, policymakers, and curious minds alike how corporate landlords can drive opportunity yet still be a point of concern to our region.

Who are corporate landlords?

Who are Corporate landlords?

The term “corporate landlord” is often applied to firms of varying sizes and types, from Limited Liability Companies (LLCs) with only a handful of properties to real estate investment trusts (REITs) with several hundred or thousand properties in various jurisdictions and markets (Goodman et al., 2023). This variation explains why these landlords are often called “investor” landlords. Regardless of what they are called, this still raises an important question: are all investor landlords the same?

CoreLogic (2023) grouped investors into four categories:

| Type of Investor | Number of Properties |

| Small (“mom-and-pop”) | 3-9 |

| Medium | 10-99 |

| Large | 100-999 |

| Mega | Over 1000 |

Contrary to what might be expected, CoreLogic (2023) found that large and mega investors accounted for a combined 20% of all investor purchases in the first quarter of 2023. Small investors, on the other hand, accounted for nearly 45% of all investor purchases during this same period. It is not always immediately clear what types of investors are purchasing properties in our communities, nor is it always clear what types of investors own the properties in our communities. In the next article in the series, we will differentiate types of investor landlords and use a unique method to identify them when that isn’t always clear in the available data (Hangen & O’Brien, 2024). For the moment, however, we will continue to use the overarching term “corporate landlord” for any type of institutional investor.

Why are corporate landlords controversial?

The increasing prominence of these landlords led to a corresponding interest in research. At first glance, some of the research appears to paint a negative impression of these owners. A study found evidence that a higher concentration of corporate landlords led to a decrease in homeownership for Black residents in the Atlanta Metro area, while Shannon, Skobba, and Durham (2023) demonstrate that properties owned by investor landlords are more likely to suffer from dilapidation. In tandem with articles linking corporate landlords to increasingly exorbitant rents (Conley, 2023) and the disproportionate eviction of minority and lower-income residents (Rios, 2022), it is not surprising that legislation has been put forward at both the federal1 and state levels2 to reign in these entities.

This does not imply that coverage around corporate landlords remains universally negative. Goodman and Golding (2021) find that, due to their advantages in accessing capital, these investors can spend anywhere from double to nearly five times the amount on renovations as the average homeowner. This can lead to improved neighborhood and housing quality. It should also be noted that the research on corporate landlords is more complicated than assumed in the previous paragraph. Recent examples include evidence that single-family rentals owned by corporate landlords can provide increased access to better neighborhoods for lower-income families (Khaleel & Hanlon, 2023) and higher-performing schools (Mayock & Vosters, 2024). In addition, Harrison, Immergluck, and Walker (2024) find evidence that institutional investors are less likely to purchase homes in neighborhoods with higher rates of poverty or homes that are in worse condition, directly contradicting Conley (2023) and Shannon et al. (2023).

One of the most common explanations for these contradictory findings stems from an issue we already mentioned and will expand upon in the next article: prior research did (could) not differentiate between different types of investor landlords.

How many corporate landlords are in Mecklenburg County?

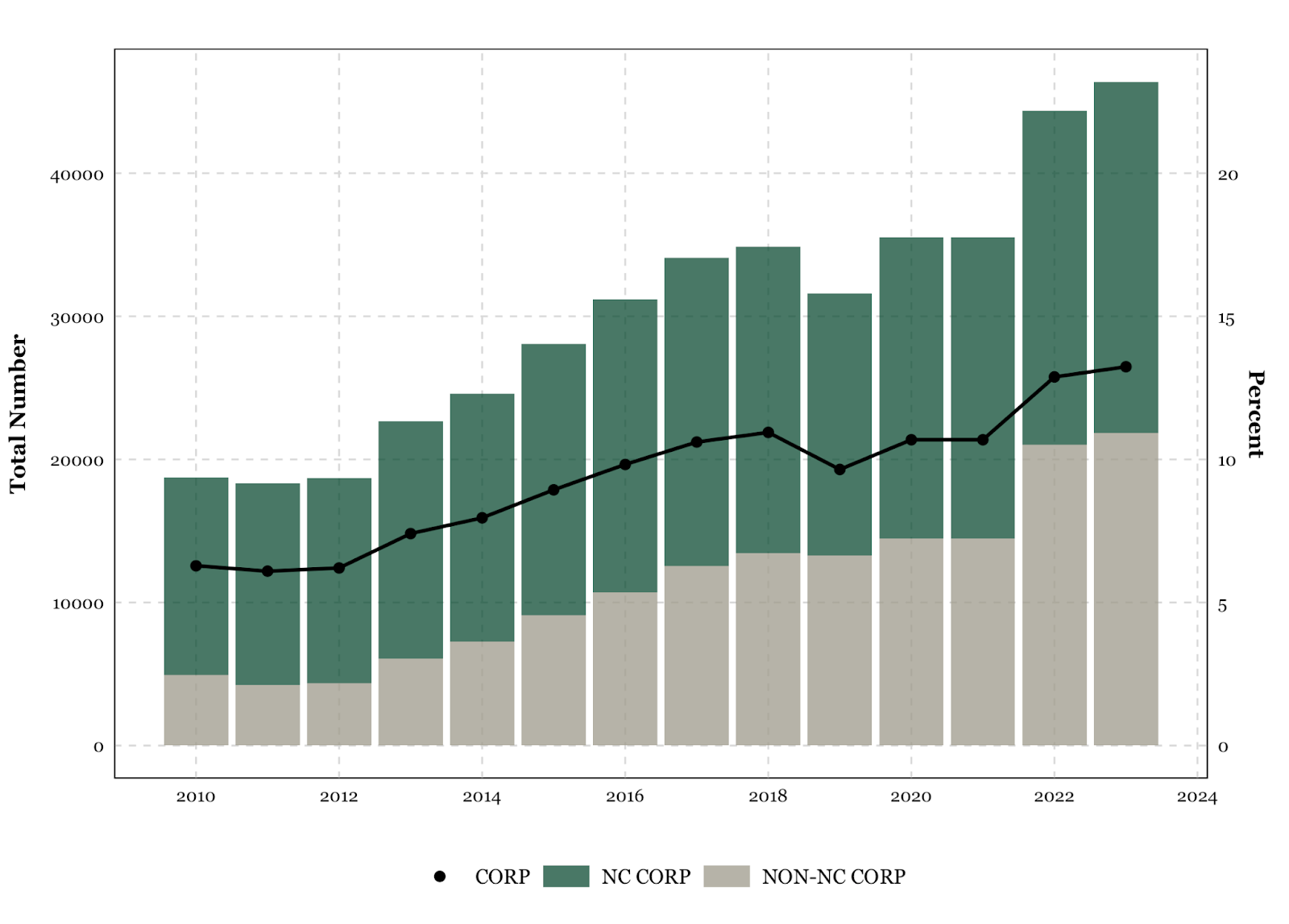

Overall, corporate landlords constitute a fraction of the owners of single-family homes. According to a recent report by The Urban Institute (2023) in Washington, D.C., these entities owned just under 600,000 homes nationwide, meaning the ownership rate of corporate landlords is estimated to be around 3.8 percent of single-family homes. In Mecklenburg County, the prevalence of corporate landlords has increased substantially in recent years. The figure below provides the total number and percentage of single-family homes that were owned by a corporation from 2010-2023.

The figure demonstrates that identified corporations owned just under 20,000 single-family homes in Mecklenburg County in 2010. This number increased to over 46,000 homes at the end of 2023, an increase of 53% (Mecklenburg County Tax Assessment Data). The overlaying line chart plots the total percentage of single-family homes owned by a corporation. Similarly, the percentage of single-family homes owned by corporations increased from approximately 10% in 2010 to around 26% in 2023.

Our analysis, which is more thoroughly explained in the next entry of this series, shows corporate landlords own approximately 22,000 homes in Mecklenburg County – roughly eight percent of available single-family housing. If these entities represent a small portion of the larger housing market, why are we so focused on them? This is a question some commentators are starting to raise as they wonder whether legislating the ability of corporations to buy single-family homes on a large scale would have any discernible impact on the housing market (Demsas, 2023; Fairweather, 2024). Others have pointed out that corporate (investor) landlords do not represent the root cause of the housing crisis; instead, focusing on the insidious impact of exclusionary zoning laws (Meyersohn, 2023).

Why is this relevant for Charlotte-Mecklenburg?

We have deliberately pointed out that corporate landlords represent only one component in the recipe for the worst housing crisis since the Great Recession. Combining this acknowledgment with the contradictory findings in the literature, the reader can be forgiven for wondering how these entities are relevant to the Charlotte-Mecklenburg area. Here’s how:

- It matters to the community: Mecklenburg County residents remain concerned with corporate landlords. In a joint study with the Lee Institute, we found evidence that a vast majority of residents believed that corporate landlords had a negative impact on their community, specifically concerning affordability, economic mobility, and community safety.

- Their impact may be concentrated: The increased presence of corporate landlords can have a disproportionate, and negative, impact on low-income and/or Black households. In addition to finding evidence that large-scale corporate investors appear to be concentrated in neighborhoods with a higher proportion of Black residents, scholars find that this concentration has resulted in a disproportionate increase in the number of evictions and a decrease in the number of minority-owned households within these neighborhoods (Raymond et al., 2021; An, 2023; Billings & Soliman, 2023; Seymour, 2023).

- The importance of homeownership: Homeownership has long been discussed as one of the primary drivers of wealth accumulation, particularly for low- and moderate-income families (Wainer & Zabel, 2020). Comparative research also finds evidence that homeowners experience higher life satisfaction levels, improved educational outcomes for dependents, and mental well-being (Acolin 2020).

These are just some of the reasons why it is important to examine corporate landlords, even if their proportion of the overall housing market may be lower than most citizens and commentators assume. The idea that corporate landlords may be concentrated in certain communities, combined with the uncertainty around identifying these entities, presents an opportunity for this series to more accurately describe the presence of corporate landlords in Mecklenburg County.

____________________________

1 Recent introduced bills include the Stop Wall Street Landlords Act of 2022 (H.R.9246), which denies certain tax and other benefits to large investors whose assets exceed $100 million in a taxable year for investment in single-family housing, and the Stop Predatory Investing Act that would restrict tax breaks for big corporate investors that buy up homes by prohibiting an investor who acquires 50 or more single-family rental homes from deducting interest or depreciation on those properties (Senate Banking Committee 2023).

2 HB 114 (2022) in North Carolina proposed limiting the total number of homes an individual or business can buy while HB1057 (2022) in Texas would have prohibited any investment firms from buying a (single-family) home until it has been on the market for 30 days.

3 This finding was consistent across the various forums (survey, interviews, and listening sessions) used to ascertain the perception that residents held around corporate landlords. It should be noted, as stated in the report, that the survey administered was not representative of Mecklenburg County and, while a diverse sample was achieved by leveraging a more targeted outreach approach via the other forums, it should provide some caution when trying to interpret or extrapolate any of the findings or conclusions from said report.

References:

- Acolin, A. (2020). Housing wealth and consumption over the 2001–2013 period: The role of the collateral channel. Journal of Housing Research, 29(1), 68-88.

- An, B. Y. (2023). The influence of institutional single-family rental investors on homeownership: Who gets targeted and pushed out of the local market? Journal of Planning Education and Research.

- Billings, S. B., & Soliman, A. (2023). The erosion of homeownership and minority wealth. Available at SSRN 4649479.

- Camp Yeakey, C. (2024). Corporate investors and the housing affordability crisis: Having Wall Street as your landlord. American Journal of Economics and Sociology.

- Conley, J. (2023, April 18). Corporate landlords reap big profits as rents in many U.S. cities soar by double digits. Salon. https://www.salon.com/2023/04/18/corporate-landlords-reap-big-profits-as-rents-in-many-us-cities-soar-by-double-digits_partner/

- Demsas, J. (2023). Meet the Latest Housing-Crisis Scapegoat. The Atlantic. https://www.theatlantic.com/ideas/archive/2023/01/housing-crisis-hedge-funds-private-equity-scapegoat/672839/

- Fairweather, D. (2024, March 6). Ban corporate landlords: A housing crisis solution or a distraction? Forbes. https://www.forbes.com/sites/darylfairweather/2024/03/05/ban-corporate-landlords-a-housing-crisis-solution-or-a-distraction/

- Goodman, L., & Golding, E. (2021). Institutional Investors Have a Comparative Advantage in Purchasing Homes That Need Repair. Urban Institute, October, 20. https://www.urban.org/urban-wire/institutional-investors-have-comparative-advantage-purchasing-homes-need-repair

- Goodman, L., Zinn, A., Reynolds, K., & Noble, E. (2023). A profile of institutional investor–owned single-family rental properties. Urban Institute.

- Hangen, F., & O’Brien, D. T. (2024). Linking landlords to uncover ownership obscurity. Housing Studies, 1-26.

- Harrison, A., Immergluck, D., & Walker, J. (2024). Single-family rental (SFR) investor types, property conditions, and implications for urban neighborhoods: evidence from Memphis, Tennessee. Housing Studies, 1-21.

- Khaleel, S., & Hanlon, B. (2023). The rise of single-family rentals and the relationship to opportunity neighborhoods for low-income families with children. Urban Studies, 60(13), 2706-2724.

- Lopez, S., Kattan, S., & Ash, J. (2022). The National Rental Home Council: How America’s Largest Single-Family Landlords Put Profit Over People. Action Center On Race and the Economy, 1996-2019.

- Malone, T. (2023, September 13). US home investor share remained high in early summer 2023. CoreLogic. https://www.corelogic.com/intelligence/us-home-investor-share-remained-high-early-summer-2023/#

- Mayock, T., & Vosters, K. (2024). Educational Achievement Gains Afforded by Moving to Single-Family Rentals. Available at SSRN 4831525.

- Mecklenburg County Assessors Office. (2024). Parcel Landuse Historical [Data set]. https://mecklenburgcounty.hosted-by-files.com/OpenMapping/Parcel%20Landuse%20Historical/

- Meyersohn, N. (2023, August 5). The invisible laws that led to America’s housing crisis | CNN business. CNN. https://www.cnn.com/2023/08/05/business/single-family-zoning-laws/index.html

- N.C. Gen. Assemb. HB 114. Reg. Sess. 2023-2024 (2023). https://www.ncleg.gov/BillLookUp/2023/H114

- Raymond, E. L., Miller, B., McKinney, M., & Braun, J. (2021). Gentrifying Atlanta: Investor purchases of rental housing, evictions, and the displacement of black residents. Housing Policy Debate, 31(3-5), 818-834.

- Rios, E. (2022, April 15). New data shows who, exactly, got evicted the most during the pandemic. Mother Jones. https://www.motherjones.com/criminal-justice/2022/04/eviction-coronavirus-racism-california/

- Seymour, E. (2023). Corporate Landlords and Pandemic and Prepandemic Evictions in Las Vegas. Housing Policy Debate, 33(6), 1368-1389.

- Seymour, E., Shelton, T., Sherman, S. A., & Akers, J. (2023). The metropolitan and neighborhood geographies of REIT-and private equity–owned single-family rentals. Journal of Urban Affairs, 1-25.

- Shannon, J., Skobba, K., & Durham, J. (2023). Landlords and Housing Quality in Rural Georgia: Assessing the Relationship. Housing Policy Debate, 1-22.

- Stop Predatory Investing Act, S.2224, 118th Congress. (2023). https://www.congress.gov/bill/118th-congress/senate-bill/2224/titles?s=1&r=92

- Stop Wall Street Landlords Act of 2022, H.R.9246, 117th Congress. (2022). https://www.congress.gov/bill/117th-congress/house-bill/9246

- Tex. Leg. HB 1057. 88(R) (2022). https://capitol.texas.gov/BillLookup/History.aspx?LegSess=88R&Bill=HB1057

- Wainer, A., & Zabel, J. (2020). Homeownership and wealth accumulation for low-income households. Journal of Housing Economics, 47, 101624.